UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

(Mark One)

For

the quarterly period ended

or

For the transition period from __________ to __________

Commission

File Number:

(Exact name of registrant as specified in its charter)

| (State or Other Jurisdiction of Incorporation or Organization) | (I.R.S. Employer Identification No.) | |

100 Park Ave., 23rd Floor New York, NY | 10017 | |

| (Address of Principal Executive Offices) | (Zip Code) |

(Registrant’s Telephone Number, Including Area Code)

(Former Address)

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol | Name of exchange on which registered | ||

Indicate

by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange

Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2)

has been subject to such filing requirements for the past 90 days. ☒

Indicate

by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule

405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant

was required to submit such files). ☒

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☐ | ||

| ☒ | Smaller reporting company | ||||

| Emerging growth company |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards, provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate

by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). ☐ Yes

Indicate the number of shares

outstanding of each of the issuer’s classes of common stock, as of May 15, 2023:

Actinium Pharmaceuticals, Inc.

Table of Contents

INDEX

| PART I – FINANCIAL INFORMATION | |||

| Item 1. | Financial Statements | 1 | |

| Item 2. | Management’s Discussion and Analysis of Financial Condition and Results of Operations | 16 | |

| Item 3. | Quantitative and Qualitative Disclosures About Market Risk | 39 | |

| Item 4. | Controls and Procedures | 39 | |

| PART II – OTHER INFORMATION | |||

| Item 1. | Legal Proceedings | 40 | |

| Item 1A. | Risk Factors | 40 | |

| Item 2. | Unregistered Sales of Equity Securities and Use of Proceeds | 71 | |

| Item 3. | Defaults Upon Senior Securities | 71 | |

| Item 4. | Mine Safety Disclosures | 71 | |

| Item 5. | Other Information | 71 | |

| Item 6. | Exhibits | 72 | |

| SIGNATURES | 73 | ||

i

PART I - FINANCIAL INFORMATION

ITEM 1. FINANCIAL STATEMENTS

The accompanying consolidated financial statements have been prepared by the Company and are unaudited. In the opinion of management, all adjustments (which include only normal recurring adjustments) necessary to present fairly the financial position at March 31, 2023 and December 31, 2022, and the results of operations and cash flows for the three months ended March 31, 2023 and 2022, respectively, have been made. Certain information and footnote disclosures normally included in financial statements prepared in accordance with accounting principles generally accepted in the United States of America have been condensed or omitted. It is suggested that these financial statements be read in conjunction with the financial statements and notes thereto included in the Company’s audited financial statements for the year ended December 31, 2022 in the Company’s Annual Report on Form 10-K. The results of operations for the three months ended March 31, 2023 are not necessarily indicative of the operating results for the full year.

1

Actinium Pharmaceuticals, Inc.

Condensed Consolidated Balance Sheets

(Unaudited)

(amounts in thousands, except share and per share data)

| March 31, 2023 | December 31, 2022 | |||||||

| (Unaudited) | ||||||||

| Assets | ||||||||

| Current Assets: | ||||||||

| Cash and cash equivalents | $ | $ | ||||||

| Restricted cash - current | ||||||||

| Prepaid expenses and other current assets | ||||||||

| Total Current Assets | ||||||||

| Property and equipment, net of accumulated depreciation of $ | ||||||||

| Restricted cash – long term | ||||||||

| Operating leases right-of-use assets | ||||||||

| Finance leases right-of-use assets | ||||||||

| Total Assets | $ | $ | ||||||

| Liabilities and Stockholders’ Equity | ||||||||

| Current Liabilities: | ||||||||

| Accounts payable and accrued expenses | $ | $ | ||||||

| Operating leases current liability | ||||||||

| Finance leases current liability | ||||||||

| Total Current Liabilities | ||||||||

| Long-term license revenue deferred | ||||||||

| Long-term operating lease obligations | ||||||||

| Total Liabilities | ||||||||

| Commitments and contingencies | ||||||||

| Stockholders’ Equity: | ||||||||

| Preferred stock, $ | ||||||||

| Common stock, $ | ||||||||

| Additional paid-in capital | ||||||||

| Accumulated deficit | ( | ) | ( | ) | ||||

| Total Stockholders’ Equity | ||||||||

| Total Liabilities and Stockholders’ Equity | $ | $ | ||||||

See accompanying notes to the condensed consolidated financial statements.

2

Actinium Pharmaceuticals, Inc.

Condensed Consolidated Statements of Operations

(Unaudited)

(amounts in thousands, except share and per share data)

For the Three Months Ended March 31 | ||||||||

| 2023 | 2022 | |||||||

| Revenue: | ||||||||

| Revenue | $ | $ | ||||||

| Other revenue | ||||||||

| Total revenue | ||||||||

| Operating expenses: | ||||||||

| Research and development, net of reimbursements | ||||||||

| General and administrative | ||||||||

| Total operating expenses | ||||||||

| Loss from operations | ( | ) | ( | ) | ||||

| Other income: | ||||||||

| Interest income - net | ||||||||

| Total other income | ||||||||

| Net loss | $ | ( | ) | $ | ( | ) | ||

| $ | ( | ) | $ | ( | ) | |||

See accompanying notes to the condensed consolidated financial statements.

3

Actinium Pharmaceuticals, Inc.

Condensed Consolidated Statement of Changes in Stockholders’ Equity

For the Period from January 1, 2023 to March 31, 2023

(Unaudited)

(amounts in thousands, except share amounts)

| Common Stock | Additional Paid-In | Accumulated | Stockholders’ | |||||||||||||||||

| Shares | Amount | Capital | Deficit | Equity | ||||||||||||||||

| Balance, January 1, 2023 | $ | $ | $ | ( | ) | $ | ||||||||||||||

| Stock-based compensation | - | |||||||||||||||||||

| Sale of common stock, net of offering costs | ||||||||||||||||||||

| Issuance of common stock from exercise of stock options | ||||||||||||||||||||

| Net loss | - | ( | ) | ( | ) | |||||||||||||||

| Balance, March 31, 2023 | $ | $ | $ | ( | ) | $ | ||||||||||||||

See accompanying notes to the condensed consolidated financial statements.

4

Actinium Pharmaceuticals, Inc.

Condensed Consolidated Statement of Changes in Stockholders’ Equity

For the Period from January 1, 2022 to March 31, 2022

(Unaudited)

(amounts in thousands, except share amounts)

| Common Stock | Additional Paid-In | Accumulated | Stockholders’ | |||||||||||||||||

| Shares | Amount | Capital | Deficit | Equity | ||||||||||||||||

| Balance, January 1, 2022 | $ | $ | $ | ( | ) | $ | ||||||||||||||

| Stock-based compensation | - | |||||||||||||||||||

| Net loss | - | ( | ) | ( | ) | |||||||||||||||

| Balance, March 31, 2022 | $ | $ | $ | ( | ) | $ | ||||||||||||||

See accompanying notes to the condensed consolidated financial statements.

5

Actinium Pharmaceuticals, Inc.

Condensed Consolidated Statements of Cash Flows

(Unaudited)

(amounts in thousands)

For

the | ||||||||

| 2023 | 2022 | |||||||

| Cash Flows Used In Operating Activities: | ||||||||

| Net loss | $ | ( | ) | $ | ( | ) | ||

| Adjustments to reconcile net loss to net cash used in operating activities: | ||||||||

| Stock-based compensation expense | ||||||||

| Depreciation & amortization expenses | ||||||||

| Changes in operating assets and liabilities: | ||||||||

| Prepaid expenses and other current assets | ( | ) | ( | ) | ||||

| Accounts payable and accrued expenses | ( | ) | ( | ) | ||||

| Other liability | ( | ) | ||||||

| Operating lease right-of-use assets | ( | ) | ||||||

| Operating lease liabilities | ( | ) | ( | ) | ||||

| Net Cash Used In Operating Activities | ( | ) | ( | ) | ||||

| Cash Flows Used In Investing Activities: | ||||||||

| Purchase of property and equipment | ( | ) | ( | ) | ||||

| Net Cash Used In Investing Activities | ( | ) | ( | ) | ||||

| Cash Flows Provided By / Used In Financing Activities: | ||||||||

| Payments on finance leases | ( | ) | ( | ) | ||||

| Sales of shares of common stock, net of costs | ||||||||

| Proceeds from the exercise of stock options | ||||||||

| Net Cash Provided By / Used In Financing Activities | ( | ) | ||||||

| Net change in cash, cash equivalents, and restricted cash | ( | ) | ( | ) | ||||

| Cash, cash equivalents, and restricted cash at beginning of period | ||||||||

| Cash, cash equivalents, and restricted cash at end of period | $ | $ | ||||||

| Supplemental disclosure of cash flow information: | ||||||||

| Cash paid for interest | $ | $ | ||||||

| Cash paid for income taxes | $ | $ | ||||||

See accompanying notes to the condensed consolidated financial statements.

6

Actinium Pharmaceuticals, Inc.

Notes to Condensed Consolidated Financial Statements

(Unaudited)

Note 1 - Description of Business and Summary of Significant Accounting Policies

Nature of Business - Actinium Pharmaceuticals, Inc. is a biopharmaceutical company developing targeted radiotherapies to deliver cancer-killing radiation with cellular level precision to treat patients with high unmet medical needs.

Basis of Presentation - Unaudited Interim Financial Information - The accompanying unaudited interim condensed consolidated financial statements and related notes have been prepared in accordance with accounting principles generally accepted in the United States of America (“U.S. GAAP”) for interim financial information, and in accordance with the rules and regulations of the United States Securities and Exchange Commission (the “SEC”) with respect to Form 10-Q and Article 10 of Regulation S-X. Accordingly, they do not include all of the information and footnotes required by U.S. GAAP for complete financial statements. The unaudited interim condensed financial statements furnished reflect all adjustments (consisting of normal recurring adjustments) which are, in the opinion of management, necessary for a fair statement of the results for the interim periods presented. Interim results are not necessarily indicative of the results for the full year. These unaudited interim condensed consolidated financial statements should be read in conjunction with the audited consolidated financial statements and notes thereto contained in the Company’s annual report on Form 10-K for the year ended December 31, 2022.

Principles of Consolidation - The basis of consolidation is unchanged from the disclosure in the Company’s Notes to the Consolidated Financial Statements section in its Report on Form 10-K for the year ended December 31, 2022. The unaudited condensed consolidated financial statements include the Company’s accounts and those of the Company’s wholly owned subsidiaries.

Use of Estimates - The preparation of these unaudited interim condensed consolidated financial statements in conformity with U.S. GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities at the date of the consolidated financial statements and the reported amounts of expenses during the reporting period. Actual results could differ from those estimates.

Cash, Cash Equivalents and Restricted Cash - The Company considers all highly liquid accounts with original maturities of three months or less to be cash equivalents. Balances held by the Company are typically in excess of Federal Deposit Insurance Corporation insured limits.

The following is a summary of cash, cash equivalents and restricted cash at March 31, 2023 and December 31, 2022:

| (in thousands) | March 31, 2023 | December 31, 2022 | ||||||

| Cash and cash equivalents | $ | $ | ||||||

| Restricted cash - current | ||||||||

| Restricted cash – long-term | ||||||||

| Cash, cash equivalents and restricted cash | $ | $ | ||||||

Restricted cash relates to certificates of deposit held as collateral for letters of credit issued in connection with the Company’s leases of corporate office spaces.

Leases – The Company has operating and finance leases for corporate office space and office equipment located at the corporate office space. Leases with an initial term of 12 months or less are not recorded on the balance sheet; lease expense for these leases is recognized on a straight-line basis over the lease term.

Fair Value Measurement - Fair value is defined as the price that would be received to sell an asset, or paid to transfer a liability, in an orderly transaction between market participants. A fair value hierarchy has been established for valuation inputs that gives the highest priority to quoted prices in active markets for identical assets or liabilities and the lowest priority to unobservable inputs.

7

Revenue Recognition - The Company recognizes revenue in accordance with Accounting Standards Codification (ASC) Topic 606, Revenue From Contracts With Customers (“ASC 606”). Under ASC 606, an entity recognizes revenue when its customer obtains control of promised goods or services, in an amount that reflects the consideration that the entity expects to receive in exchange for those goods or services. To determine revenue recognition for arrangements within the scope of ASC 606, the entity performs the following five steps: (i) identify the contract(s) with a customer; (ii) identify the performance obligations in the contract; (iii) determine the transaction price, including variable consideration, if any; (iv) allocate the transaction price to the performance obligations in the contract; and (v) recognize revenue as the entity satisfies a performance obligation. The Company only applies the five-step model to contracts when it is probable that the entity will collect the consideration to which it is entitled in exchange for the goods or services it transfers to the customer.

At contract inception, once the contract is determined to be within the scope of ASC 606, the Company assesses whether the promised goods or services promised within each contract are distinct and, therefore, represent a separate performance obligation. Goods and services that are determined not to be distinct are combined with other promised goods and services until a distinct bundle is identified. In determining whether goods or services are distinct, the Company evaluates certain criteria, including whether (i) the customer can benefit from the good or service either on its own or together with other resources that are readily available to the customer (capable of being distinct) and (ii) the good or service is separately identifiable from other goods or services in the contract (distinct in the context of the contract).

The Company then determines the transaction price, which is the amount of consideration it expects to be entitled from a customer in exchange for the promised goods or services for each performance obligation and recognizes the associated revenue as each performance obligation is satisfied. The Company’s estimate of the transaction price for each contract includes all variable consideration to which it expects to be entitled. Variable consideration includes payments in the form of collaboration milestone payments. If an arrangement includes collaboration milestone payments, the Company evaluates whether the milestones are considered probable of being reached and estimates the amount to be included in the transaction price using the most likely amount method. If it is probable that a significant revenue reversal would not occur, the associated milestone value is included in the transaction price.

ASC 606 requires the Company to allocate the arrangement consideration on a relative standalone selling price basis for each performance obligation after determining the transaction price of the contract and identifying the performance obligations to which that amount should be allocated. The relative standalone selling price is defined in the revenue standard as the price at which an entity would sell a promised good or service separately to a customer. The Company then recognizes as revenue the amount of the transaction price that is allocated to the respective performance obligation as each performance obligation is satisfied, either at a point in time or over time, and if over time, recognition is based on the use of an output or input method.

Collaborative Arrangements - The Company follows the accounting guidance for collaboration agreements with third parties, which requires that certain transactions between the Company and collaborators be recorded in its consolidated statements of operations on either a gross basis or net basis, depending on the characteristics of the collaborative relationship, and requires enhanced disclosure of collaborative relationships. The Company evaluates its collaboration agreements for proper classification in its consolidated statements of operations based on the nature of the underlying activity. When the Company has concluded that it has a customer relationship with one of its collaborators, the Company follows the guidance of ASC 606.

Grant Revenue – The Company had a grant from a government-sponsored entity for research and development related activities that provided for payments for reimbursed costs, which included overhead and general and administrative costs as well as an administrative fee. The Company recognized revenue from grants as it performed services under this arrangement. Associated expenses were recognized when incurred as research and development expense. Revenue and related expenses are presented gross in the consolidated statements of operations.

8

License Revenue – The Company entered into a product licensing agreement whereby the Company allowed a third party to commercialize a certain product in specified territories using the Company’s trademarks. The terms of this arrangement includes payment to the Company for a combination of one or more of the following: upfront license fees; development, regulatory and sales-based milestone payments; and royalties on net sales of licensed products. The Company uses its judgment to determine whether milestones or other variable consideration should be included in the transaction price.

Upfront license fees: If the license to the Company’s intellectual property is determined to be distinct from the other performance obligations identified in the arrangement, the Company will recognize revenue from upfront license fees allocated to the license when the license is transferred to the licensee and the licensee is able to use and benefit from the license. For licenses that are bundled with other promises, the Company determines whether the combined performance obligation is satisfied over time or at a point in time.

Development, regulatory or commercial milestone payments: At the inception of each arrangement that includes payments based on the achievement of certain development, regulatory and sales-based or commercial events, the Company evaluates whether the milestones are considered probable of being achieved and estimates the amount to be included in the transaction price using the most likely amount method. If it is probable that a significant revenue reversal would not occur, the associated milestone value is included in the transaction price. Milestone payments that are not within the Company’s or the licensee’s control, such as regulatory approvals, are not considered probable of being achieved until regulatory approval is received. At the end of each subsequent reporting period, the Company will re-evaluate the probability of achieving such development and regulatory milestones and any related constraint, and if necessary, adjust the Company’s estimate of the overall transaction price. Any such adjustments are recorded on a cumulative catch-up basis and recorded as part of license revenue during the period of adjustment.

Sales-based milestone payments and royalties: For arrangements that include sales-based royalties, including milestone payments based on the volume of sales, the Company will determine whether the license is deemed to be the predominant item to which the royalties or sales-based milestones relate and if such is the case, the Company will recognize revenue at the later of (i) when the related sales occur, or (ii) when the performance obligation to which some or all of the royalty has been allocated has been satisfied (or partially satisfied).

Upfront payments and fees may require deferral of revenue recognition to a future period until the Company performs its obligations under these arrangements or when it is probable that a significant reversal in the amount of cumulative revenue recognized will not occur or when the uncertainty associated with any variable consideration is subsequently resolved. Amounts payable to the Company are recorded as accounts receivable when the Company’s right to consideration is unconditional.

Research and Development Costs - Research and development costs are expensed as incurred. These costs include the costs of manufacturing drug product, the costs of clinical trials, costs of employees and associated overhead, and depreciation and amortization costs related to facilities and equipment. Research and development reimbursements are recorded by the Company as a reduction of research and development costs.

Share-Based Payments - The Company estimates the fair value of each stock option award at the grant date by using the Black-Scholes option pricing model. The fair value determined represents the cost for the award and is recognized over the vesting period during which an employee is required to provide service in exchange for the award. The Company accounts for forfeitures of stock options as they occur.

9

Net Loss Per Common Share - Basic loss per common share is computed by dividing the net loss available to common stockholders by the weighted average number of shares of common stock outstanding during the reporting period. For periods of net loss, diluted loss per share is calculated similarly to basic loss per share because the impact of all potential dilutive common shares is anti-dilutive. For the three and nine months ended March 31, 2023 and 2022, the Company’s potentially dilutive shares, which include outstanding common stock options, restricted stock units and warrants, have not been included in the computation of diluted net loss per share as the result would have been anti-dilutive.

| (in thousands) | March 31, 2023 | March 31, 2022 | ||||||

| Options | ||||||||

| Restricted Stock Units | ||||||||

| Warrants | ||||||||

| Total | ||||||||

Recently Adopted Accounting Pronouncements – In November 2021, the FASB issued ASU 2021-10, Government Assistance (Topic 832), Disclosures by Business Entities about Government Assistance, which provides guidance on disclosure requirements to entities other than not-for-profit entities about transaction with a government that are accounted for by applying a grant or contribution accounting model by analogy. ASU 2021-10 requires an entity to make annual disclosures related to (1) the nature of the transactions and the related accounting policy used to account for the government transactions, (2) quantification and disclosure of amounts related to the government transactions included in balance sheet and income statement financial statement line items, and (3) significant terms and conditions of the government transactions, including commitments and contingencies. The amendments of ASU 2021-10 are effective January 1, 2022, including interim periods. The Company adopted this standard effective January 1, 2022, and the standard did not have a material impact on the Company’s financial statements.

In October 2021, FASB issued ASU 2021-08, Business Combinations (Topic 805), Account for Contract Assets and Contract Liabilities from Contracts with Customers, which provides guidance on accounting for contract assets and contract liabilities acquired in a business combination in accordance with ASC 606. To achieve this, an acquirer may assess how the acquiree applied ASC 606 to determine what to record for the acquired revenue contracts. Generally, this should result in an acquirer recognizing and measuring the acquired contract assets and contract liabilities consistent with how they were recognized and measured in the acquiree’s financial statements. The amendments of ASU 2021-08 are effective January 1, 2023, including interim periods. The Company will evaluate the impact of ASU 2021-08 on any future business combinations the Company may enter in the future.

In May 2021, FASB issued ASU 2021-04, Earnings Per Share (topic 260), Debt — Modifications and Extinguishments (Subtopic 470-50), Compensation – Stock Compensation (Topic 718) and Derivatives and Hedging – Contracts in an Entity’s Own Equity (Subtopic 815-40) – Issuer’s Accounting for Certain Modifications or Exchanges of Freestanding Equity-Classified Written Call Options, which provides guidance of a modification or an exchange of a freestanding equity-classified written call option that remains equity classified after modification or exchange as (1) an adjustment to equity and, if so, the related earnings per share (EPS) effects, if any, or (2) an expense and, if so, the manner and pattern of recognition. The amendments in this ASU are effective January 1, 2022, including interim periods. The Company adopted this standard effective January 1, 2022 and the standard did not have a material effect on the Company’s financial statements.

Note 2 - Commitments and Contingencies

On June 15, 2012, the Company

entered into a license and sponsored research agreement with Fred Hutchinson Cancer Research Center (“FHCRC”) to build upon

previous and ongoing clinical trials with apamistamab (licensed antibody). FHCRC has completed both a Phase 1 and Phase 2 clinical trial

with apamistamab. The Company has been granted exclusive rights to the antibody and related master cell bank developed by FHCRC. A milestone

payment of $

10

Note 3 - Leases

The Company determines if an arrangement is a lease at inception. This determination generally depends on whether the arrangement conveys to the Company the right to control the use of a fixed asset for a period of time in exchange for consideration. Control of an underlying asset is conveyed to the Company if the Company obtains the rights to direct the use of and to obtain substantially all of the economic benefits from using the underlying asset. The Company has lease agreements which include lease and non-lease components, which the Company has elected to account for as a single lease component for all classes of underlying assets. Lease expense for variable lease components are recognized when the obligation is probable. The Company made an accounting policy election to exclude from balance sheet reporting those leases with initial terms of 12 months or less.

Right-of-use assets and liabilities are recognized at commencement date based on the present value of lease payments over the lease term. ASC 842 requires a lessee to discount its unpaid lease payments using the interest rate implicit in the lease or, if that rate cannot be readily determined, its incremental borrowing rate. As an implicit interest rate was not readily determinable in the Company’s leases, the incremental borrowing rate was used based on the information available at commencement date in determining the present value of lease payments.

The lease term for all of the Company’s leases includes the non-cancellable period of the lease plus any additional periods covered by either a Company option to extend (or not to terminate) the lease that the Company is reasonably certain to exercise, or an option to extend (or not to terminate) the lease controlled by the lessor. Options for lease renewals have been excluded from the lease term (and lease liability) for the majority of the Company’s leases as the reasonably certain threshold is not met.

The Company entered into a

lease for corporate office space effective June 1, 2022. The lease has a term of

The components of lease expense are as follows:

| Three months ended | ||||||||

| (in thousands) | March 31, 2023 | March 31, 2022 | ||||||

| Operating lease expense | $ | $ | ||||||

| Finance lease cost | ||||||||

| Amortization of right-to-use assets | $ | $ | ||||||

| Interest on lease liabilities | $ | $ | ||||||

| Total finance lease cost | $ | $ | ||||||

Supplemental cash flow information related to leases are as follows:

| Cash flow information: | Three months ended | |||||||

| (in thousands) | March 31, 2023 | March 31, 2022 | ||||||

| Cash paid for amounts included in the measurement of lease liabilities: | ||||||||

| Operating cash flow use from operating leases | $ | $ | ||||||

| Operating cash flow use from finance leases | $ | $ | ||||||

| Financing cash flow use from finance leases | $ | $ | ||||||

| Non-cash activity: | ||||||||

| Right-of-use assets obtained in exchange for lease obligations: | ||||||||

| Operating leases | $ | $ | ||||||

| Finance Leases | $ | $ | ||||||

11

Weighted average remaining lease terms are as follows at March 31, 2023:

| Weighted average remaining lease term: | ||||

| Operating leases | ||||

| Finance Leases |

As the interest rate implicit in the leases was not readily determinable at the time that the leases were evaluated, the Company used its incremental borrowing rate based on the information available in determining the present value of lease payments. The Company’s incremental borrowing rate was based on the term of the lease, the economic environment of the lease and reflects the rate the Company would have had to pay to borrow on a secured basis. Below is information on the weighted average discount rates used at the time that the leases were evaluated:

| Weighted average discount rates: | ||||

| Operating leases | % | |||

| Finance Leases | % | |||

Maturities of lease liabilities are as follows:

| (in thousands) Year ending December 31, | Operating Leases | Finance Leases | ||||||

| 2023 (excluding three months ended March 31, 2023) | $ | $ | ||||||

| 2024 | ||||||||

| 2025 | ||||||||

| 2026 | ||||||||

| 2027 | ||||||||

| Total lease payments | $ | $ | ||||||

| Less imputed interest | ( | ) | ||||||

| Present value of lease liabilities | $ | $ | ||||||

Note 4 – Other revenue

The Company determined that

certain collaborations with a third party are within the scope of ASC 606. The collaboration agreement is made up of multiple modules

related to various research activities. The Company identified a single performance obligation to provide research services within each

module for which the Company receives monetary consideration. The third party can choose to proceed with each module or can terminate

the agreement at any time. The Company recognizes revenue for each module on a straight-line basis over the expected module period. Revenue

for succeeding modules is not recognized until all contingencies are resolved, inclusive of the third party’s ability to terminate

the module. The consideration is recognized as revenue over each module and revenue of $

The Company had a grant

from a government-sponsored entity for research and development related activities that provides payments for reimbursed costs,

which included overhead and general and administrative costs, as well as an administrative fee. The Company recognized revenue from

grants as it performed services under this arrangement. Associated expenses are recognized when incurred as research and development

expense. Other revenue recognized from this grant for the three months ended March 31, 2022 was $

12

On April 7, 2022, the Company

entered into a license and supply agreement (the “License Agreement”) with Immedica Pharma AB (“Immedica”), pursuant

to which Immedica licensed the exclusive product rights for commercialization of Iomab-B (I-131 apamistamab) in the European Economic

Area, Middle East and North Africa (EUMENA) including Algeria, Andorra, Bahrain, Cyprus, Egypt, Iran, Iraq, Israel, Jordan, Kuwait, Lebanon,

Libya, Monaco, Morocco, Oman, Palestine, Qatar, San Marino, Saudi Arabia, Switzerland, Syria, Tunisia, Turkey, the United Arab Emirates,

the United Kingdom, the Vatican City and Yemen. Upon signing, the Company was entitled to an upfront payment of $

The Company’s contract

liabilities are recorded within Other revenue deferred – current liability or Long-term license revenue deferred in its condensed

consolidated balance sheets, depending on the short-term or long-term nature of the payments to be recognized. The Company’s contract

liabilities primarily consist of advanced payments from licensees. There was no Other revenue deferred – current liability at March

31, 2023 and December 31, 2022. Long-term license revenue deferred was $

Note 5 - Equity

In August 2020, the Company

entered into the Capital on Demand™ Sales Agreement with JonesTrading Institutional Services LLC, or JonesTrading, pursuant to which

the Company may sell, from time to time, through or to JonesTrading, up to an aggregate of $

For the three months ended

March 31, 2023, the Company sold

13

Stock Options

The following is a summary of stock option activity for the three months ended March 31, 2023:

| (in thousands, except for per-share amounts) | Number of Shares | Weighted Average Exercise Price ($) | Weighted Average Remaining Contractual Term (in years) | Aggregate Intrinsic Value | ||||||||||||

| Outstanding, January 1, 2023 | $ | $ | ||||||||||||||

| Granted | ||||||||||||||||

| Exercised | ( | ) | ||||||||||||||

| Cancelled | ( | ) | ||||||||||||||

| Outstanding, March 31, 2023 | ||||||||||||||||

| Exercisable, March 31, 2023 | ||||||||||||||||

During the three months ended

March 31, 2023, the Company granted new employees options to purchase

The fair values of all options

issued and outstanding are being amortized over their respective vesting periods. The unrecognized compensation expense at March 31, 2023

was $

Restricted Stock Units

The following is a summary of restricted stock unit activity for the three months ended March 31, 2023:

| (in thousands, except for per-share amount) | RSUs | Weighted Average Grant date Fair Value Per Share ($) | ||||||

| Outstanding, January 1, 2023 | ||||||||

| Granted | ||||||||

| Vested | ||||||||

| Outstanding, March 31, 2023 | ||||||||

The RSUs vest at the earliest

of a change of control event, the termination of the recipient’s continuous service status for any reason other than by the Company

for cause and the third anniversary of the date of the grant. The fair value of the RSUs, $

14

Warrants

Following is a summary of warrant activity for the three months ended March 31, 2023:

| (in thousands, except for per-share amounts) | Number of Shares | Weighted Average Exercise Price ($) | Weighted Average Remaining Contractual Term (in years) | Aggregate Intrinsic Value | ||||||||||||

| Outstanding, January 1, 2023 | $ | $ | ||||||||||||||

| Granted | ||||||||||||||||

| Expired | ||||||||||||||||

| Outstanding, March 31, 2023 | $ | $ | ||||||||||||||

| Exercisable, March 31, 2023 | $ | $ | ||||||||||||||

Note 6 - Subsequent Event

Since March 31, 2023, the

Company has sold

15

ITEM 2. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATION

FORWARD-LOOKING STATEMENT NOTICE

This Form 10-Q contains certain forward-looking statements. For this purpose, any statements contained in this Form 10-Q that are not statements of historical fact may be deemed to be forward-looking statements. Without limiting the foregoing, words such as “may,” “will,” “expect,” “believe,” “anticipate,” “estimate” or “continue” or comparable terminology are intended to identify forward-looking statements. These statements by their nature involve substantial risks and uncertainties, and actual results may differ materially depending on a variety of factors, many of which are not within our control. These factors include but are not limited to economic conditions generally and in the industries in which we may participate; competition within our chosen industry, including competition from much larger competitors; technological advances and failure to successfully develop business relationships.

Description of Business

Actinium Pharmaceuticals, Inc. (“Actinium”) is a biopharmaceutical company developing targeted radiotherapies to deliver cancer-killing radiation with cellular level precision to treat patients with high unmet medical needs. Our vision is to build a specialty, hospital focused, radiotherapeutics company that develops and markets medicines for relapsed or refractory cancer patients who are treated primarily in large quaternary care hospitals and their catchment areas. We intend to leverage the clinical data of our lead product candidates, Iomab-B and Actimab-A, to improve outcomes in patients with relapsed or refractory acute myeloid leukemia (“r/r AML”) by launching two radiotherapy drugs over the next several years to address the significant need for better outcomes from treatment with therapeutics or from undergoing a bone marrow transplant (“BMT”).

We also intend to further advance Iomab-B outside of acute myeloid leukemia (“AML”) based on promising data as a disease control and conditioning agent for various other blood cancers. Based on early promising clinical trial results, we are also working on a lower dose, next generation conditioning program, Iomab-ACT, for rapidly growing cell and gene therapies.

Our Clinical Pipeline

AML is an aggressive, heterogeneous disease that is difficult-to-treat. Most AML patients develop relapsed or refractory disease within one year of being afflicted and have an extremely poor prognosis and dismal survival. Currently, a BMT is the only curative regimen available for AML patients, however, access is limited to AML patients who are fit enough to withstand the challenges associated with this treatment. The majority of AML patients are considered not transplantable in routine clinical practice as they are not fit enough to withstand the rigors of the patient journey which includes therapy to attain a remission, conditioning regimens to destroy diseased marrow, challenge of the transplant itself or post-transplant complications.

16

Our Iomab-B and Actimab-A product candidates potentially fill the major unmet medical needs in r/r AML in a complementary fashion as they are directed at different parts of the patient journey. Iomab-B is being developed as a targeted bridging therapy candidate that we believe could provide both disease control and conditioning in one agent. We believe results from a Phase 3 trial demonstrate the possibility for unprecedented access to a BMT and improved survival in unfit patients who are currently not considered transplantable in routine clinical practice. We are developing Actimab-A as a targeted therapy candidate for fit patients that has demonstrated an extension in survival in a proof-of-concept study and is poised for advanced development in collaboration with the NCI, or National Cancer Institute. Together, we believe these two product candidates could provide us the opportunity to transform the treatment of AML, especially in the relapsed and refractory segment which represents over 50% of AML patients.

We announced in October 2022 that Iomab-B met the primary endpoint of durable Complete Remission (“dCR”) with a high degree of statistical significance (p<0.0001) in the pivotal Phase 3 Study of Iomab-B in Elderly Relapsed or Refractor AML, or “SIERRA trial.” In February 2023, we announced full trial results, demonstrating unprecedented transplant access and improved outcomes in patients with relapsed/refractory AML, with double 1-year and median overall survival (“OS”) compared to control arm patients. These data were presented at the 2023 Tandem Meetings aka the Transplantation & Cellular Therapy Meetings of the American Society for Transplantation and Cellular Therapy (“ASTCT”) and the Center for International Blood & Marrow Transplant Research (“CIBMTR”). We believe these results from the SIERRA trial may provide the opportunity, if we are able to obtain FDA approval, to establish Iomab-B as a new standard of care.

The results from the SIERRA trial were recently presented and discussed at major oncology medical and nursing congresses, which is helping to broaden the awareness of Iomab-B among members of the relevant medical and scientific communities as we prepare for potential commercialization if we achieve FDA approval. On April 27, 2023, the results from the SIERRA trial were also showcased at the European Society for Blood and Marrow Transplantation (“EBMT”) 49th Annual Meeting, which is well-attended by the European transplant community. On April 28, 2023, we announced that two posters that detailed clinical findings from the SIERRA trial sites were presented at the 48th Annual Oncology Nursing Society (“ONS”) Congress. We believe that the scientific community present at such events took note of the successful administration of Iomab-B infusions at various BMT centers, which was done without increasing radiation exposure risks to treating nursing staff. On May 11, 2023, we announced that these results were also accepted for oral presentation at the European Hematology Association (“EHA”) 2023 Hybrid Congress to be held in Frankfurt, Germany on June 8-11, 2023.

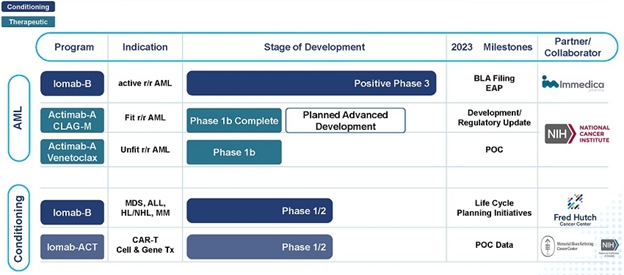

We are working towards completing and submitting our Biologics License Application (“BLA”) for Iomab-B to the U.S. Food and Drug Administration (“FDA”) in the second half of 2023 and if approved, we intend to commercialize Iomab-B in the U.S.

We are committed to bringing Iomab-B to patients globally and are working with Immedica AB (“Immedica”), our European, Middle East and North Africa (“EUMENA”) partner, for the subsequent marketing authorization application (“MAA”) of Iomab-B with the European Medicines Agency (“EMA”). Europe represents a large commercial market opportunity with approximately twice as many transplants performed in Europe compared to the U.S.

Actimab-A is being developed under what we believe to be the current industry-leading clinical-study program utilizing the potent alpha radiation emitting isotope Actinium-225 (“Ac-225”) with clinical data in approximately 150 patients treated over 6 clinical trials. The potent linear energy transfer emitted by Ac-225 has no known resistance mechanism. Actimab-A is being developed in combination with other regimens to exploit mechanistic synergies and leverage the mutation-agnostic mechanism of action of Ac-225 with the objective of establishing it as a backbone therapy in AML, an extremely heterogenous disease.

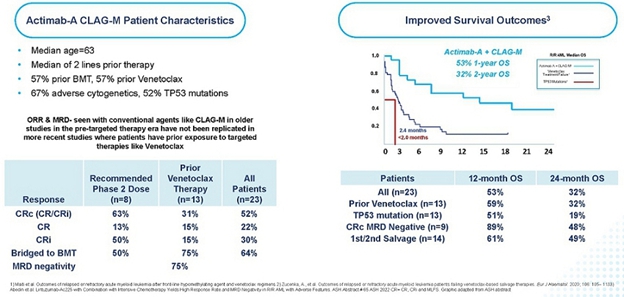

We believe our Actimab-A + CLAG-M therapeutic combination trial results in r/r AML provide validation of this approach, which such results were presented at the American Society of Hematology (“ASH”) 2022 Annual Meeting & Exposition in December 2022. Phase 1 results from the Actimab-A + CLAG-M combination trial showed high response rates and minimal residual disease (“MRD”) negativity, translating to a survival benefit of 53% and 32% at one and two years in patients who are typically expected to live two to four months. At the same meeting, we shared Phase 1 data showing that the combination of Actimab-A + venetoclax was well-tolerated with responses, including a Complete Remission (“CR”) and a partial response in early dose escalation cohorts. We believe the promise of these results may pave the way for the NCI Cooperative Research and Development Agreement (“CRADA”), announced on February 6, 2023, to develop Actimab-A for the treatment of patients with AML and other hematologic malignancies.

To explore the potential for a broader development opportunity with our Actimab-A program, we are studying the potential use of Actimab-A in solid tumor indications through our R&D efforts. CD33-expressing myeloid derived suppressor cells (“MDSCs") are present within the tumor microenvironment and exert immunosuppressive effects. On April 18, 2023, we presented preclinical data at the Association for Cancer Research (“AACR”) Annual Meeting that depicted Actimab-A’s role in the tumor microenvironment to overcome immunosuppression driven by MDSCs. We believe that our findings thus far show Actimab-A’s potential to selectively deplete MDSCs in lung and colorectal cancer. Actimab-A also demonstrated superior depletion of human MDSCs compared to Mylotarg, a CD33-targeted antibody-drug conjugate (“ADC”) in colorectal cancer (p<0.01), highlighting the powerful cytotoxicity and potential therapeutic benefit of radiotherapy compared to naked antibodies or ADCs. We believe that the data we have gathered to-date continues to support our objective to demonstrate the potential for Actimab-A to be a backbone therapy to broadly improve antitumor activity of immunotherapies and other therapeutic modalities.

Our differentiated R&D efforts are further exemplified by our next-generation Iomab-ACT conditioning program for rapidly growing cell and gene therapies, as well as our solid tumor and immunotherapy collaborations with Astellas Pharma Inc. (“Astellas”), AVEO Oncology/LG Chem (“LG Chem”) and EpicentRx, Inc. (“EpicentRx”). We have several ongoing programs in solid tumors at the pre-clinical stage with investigational new drug (“IND”) enabling studies underway.

17

Our platform has been used to develop a pipeline of novel radiotherapeutic assets to drive company growth. Preclinical pharmacology studies with our targeted radiotherapeutics such as HER3-ARC, HER2-ARC or CD33-ARC have shown strong improvement in tumor growth inhibition in various preclinical tumor models as single agents or in combination with immunotherapy such as magrolimab, an anti-CD47 monoclonal antibody. These results have prompted the team to spearhead efforts in multiple solid tumor programs.

Actinium’s lead solid tumor program is a targeted radiotherapy against HER3, a pan-cancer target that is overexpressed in several solid tumor indications with high unmet need. We have aligned our R&D strategy of advancing solid tumors into the clinic with our Actimab-A program. We recently presented pre-clinical data at the AACR 2023 Annual Meeting, highlighting this opportunity. We believe the results support further testing to evaluate the anti-tumor effects of HER3-targeted radiotherapy. HER3 conjugated to either alpha-emitting Ac-225 or beta-emitting Lutetium-177 (“Lu-177”) displayed anticancer activity in ovarian and colorectal cancer preclinical models. The consistent overexpression of HER3 in multiple solid tumor types, including ovarian, renal, prostate, urothelial, breast, and lung cancers suggests broad utility of a HER3-targeted agent in a clinical setting, which we intend to explore further. In addition, our intellectual property (“IP”) portfolio includes over 200 issued patents and pending patent applications worldwide

We are actively working on launching an early access program (“EAP”) for Iomab-B and intend to file a BLA by year-end while preparing for a U.S. commercial launch, if such BLA is approved by FDA, and working with our partner Immedica to support the Marketing Authorization Application (“MAA”) and, if approved by EMA, commercialization in the EU. Late-stage Actimab-A development is expected to begin in the second half of 2023 under the NCI CRADA. With the approximately $94.5 million cash on hand as of March 31, 2023, we expect to fund operations through 2025 as we continue to drive ahead with realizing our five-year plan.

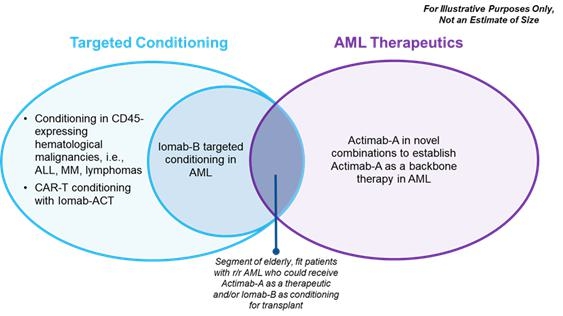

Market Opportunity

The market opportunity for Iomab-B and Actimab-A, as depicted in the diagram below, exists in AML and for cellular therapy conditioning in various blood cancers. We believe that Iomab-B and Actimab-A can fill the major unmet medical needs in r/r AML in a complementary fashion as they are utilized in different parts of the patient treatment journey. The incidence of AML is approximately 21,000 patients per year, with a prevalence of approximately 70,000 in the U.S., (approximately 27,500 new patients per year in Europe) and the disease has an outsized economic impact relative to its population size. Over 50% of patients diagnosed with AML will develop relapsed or refractory disease, with a median age of 68 years at diagnosis. Despite 10 new approved therapies since 2017, no significant advancements have been made toward a cure and there is an important unmet medical need for better therapeutics, which provide the opportunity for Actimab-A. Actimab-A is a targeted radiotherapy for fit patients that has demonstrated an impressive improvement in survival in a proof-of-concept study and is poised for advanced development in collaboration with the NCI. Using Actimab-A in combination with chemotherapy or a targeted therapy, we have the potential opportunity to treat both newly diagnosed or r/r AML patients, with the potential addressable population comparable to the prevalence of patients with AML.

18

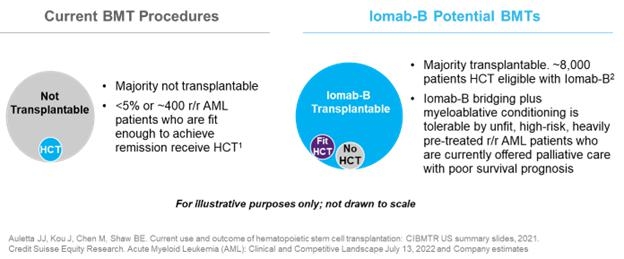

Today, less than 20% of AML patients are able to access a BMT, currently the only potentially curative option. These patients are usually younger, fit, and able to withstand the challenges associated with this treatment, leaving the large majority of AML patients ineligible for transplant. This provides an opportunity for Iomab-B, which has demonstrated the ability to enable unfit patients to benefit from a BMT. Thus Iomab-B can potentially expand the market from the approximately 400 r/r AML patients who are transplanted currently to approximately 8,000 unfit patients that could be eligible for transplant. Iomab-B has demonstrated the ability to improve BMT access with extended survival and potentially curative outcomes in several other hematological diseases outside of AML. Several clinical trials in over 300 patients with myelodysplastic syndromes (“MDS”), acute lymphocytic leukemia (“ALL”), Hodgkin’s lymphoma (“HL”), Non-Hodgkin lymphoma (“NHL”) and multiple myeloma (“MM”) have demonstrated the same value proposition as in AML. This data provides a potential opportunity to expand the market for Iomab-B beyond AML via label expansion. In the U.S., there are approximately 185,000 patients diagnosed annually with blood cancers (e.g., leukemia, lymphoma, and myeloma) that are treatable with BMT, of which, approximately 20,000 are transplanted, leaving greater than 165,000 patients who could potentially benefit from transplant. These patients do not receive a BMT today primarily because they are unfit with active disease and are not considered eligible, as they cannot tolerate the rigors of therapy required to induce a remission and the conditioning agents required to ablate the marrow prior to a BMT.

Beyond BMT, the opportunity exists for better conditioning in other areas of cellular therapy such as CAR-T as well as gene therapies. The pipeline of CAR-T and gene therapies has rapidly expanded, with the addressable patient population expected to nearly double in the next one to five years and reach approximately 93,000 patients in the U.S. by 2030 based on the current pipeline of cellular therapies. The CAR-T market size in terms of dollars is estimated to grow at a CAGR of approximately 11% over the next 5 plus years. The addressable market for Iomab-ACT is in line with the patient population for cellular therapy as all patients receive conditioning of some type prior to these treatments. We will continue to develop Iomab-ACT, our lower dose, next generation conditioning program for rapidly growing cell and gene therapies based on early promising results, ultimately with the value proposition of improving overall access and outcomes for patients who need cellular or gene therapies.

Our Strategy

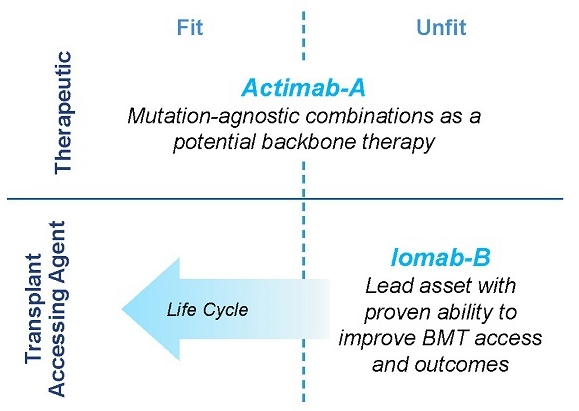

Actinium’s strategy is to build a fully integrated, specialty radiotherapeutics company focused on the top 100 cancer hospitals using the power of our platform to deliver new treatment options for patient populations living with high unmet medical needs in hematology and oncology. We believe our focus on relapsed and refractory disease in cancer indications with high unmet medical need, with limited or no competition, and where the primary delivery of care occurs in large comprehensive cancer care centers, is the appropriate strategy for our company. The cell killing power of linear energy transfer delivered via radiotherapeutics is unmatched by other technologies and we believe relapsed, refractory disease is an area where radiotherapeutics can succeed over other approaches. However, radiotherapeutics must be delivered on a just-in-time basis, and commercial and supply chain barriers are higher than with other types of medicines. The validity of our approach is demonstrated by our product development strategy as well as the commercial and operating model that we are building for our lead product candidates, Iomab-B and Actimab-A.

We intend to transform the treatment of AML with our Iomab-B and Actimab-A product candidates, each of which has demonstrated extension of survival in the most difficult-to-treat patients who are typically expected to survive for two to four months. The r/r AML segment comprises over 50% of all AML patients. Actimab-A, a therapeutic agent, and Iomab-B for induction and conditioning, can be used in a complementary fashion as depicted in the diagram below. Based on solid clinical evidence with these product candidates, we intend to develop and commercialize these two radiotherapy drugs, starting with Iomab-B in 2024 and Actimab-A in 2027, if approved, to improve survival in patients with r/r AML.

19

Iomab-B and Actimab-A have the potential to significantly improve r/r AML outcomes in a complementary manner

The operating model required to achieve our vision is attractive for several reasons, including the concentrated point of care; the top 50 transplant centers account for approximately 75% of BMTs and the top 100 hospitals treat over 50 percent of r/r AML patients. Further, there is significant overlap in the healthcare providers and ecosystem required to diagnose, treat and care for r/r AML patients within these hospitals, which will enable us to deploy a relatively small commercial organization and operate a supply chain without the need for large investments. Our product pipeline is targeting a broader opportunity in conditioning via label expansion of Iomab-B into BMT for other blood cancers and with Iomab-ACT, our next generation conditioning program for rapidly growing cell and gene therapies. Further, our solid tumor programs are initially directed at relapsed or refractory cancers, a stage of disease where treatment is again concentrated in large hospitals, which account for a significant portion of patients. We believe our strategy will enable us to build a successful company with high operating efficiencies and is feasible to achieve without requiring a commercial partner.

Our strategic priorities are to:

| ● | Establish Iomab-B as the standard of care to improve BMT access and survival outcomes in r/r AML patients who are currently not considered transplantable in routine clinical practice: We intend to file a BLA in the second half of 2023 based on the positive results from the Pivotal Phase 3 SIERRA trial and leverage our operating track record at key cancer centers to build an organization that can effectively commercialize Iomab-B. By virtue of the SIERRA trial, we have established operations at 24 leading BMT centers that represent about 30% of transplant volume in the U.S. and have strong working partnership with Key Opinion Leaders and their teams. The SIERRA results demonstrating unprecedented access to BMT and outcomes along with our commitment to operational excellence provides a strong foundation for our commercial team in the U.S. We will also work with our partner Immedica to file the MAA for the EU and support Iomab-B’s potential approval and launch with our expertise, as well as supply drug product for commercialization. |

| ● | Advance Actimab-A in combinations as a backbone therapy for r/r AML: We intend to progress late-stage development of Actimab-A to leverage its mutation-agnostic mechanism of action and exploit synergies in combination with other treatments to develop it as an AML backbone therapy. This approach is validated by proof-of-concept data from our Actimab-A + CLAG-M combination trial in r/r AML, which included 57% of patients who had failed venetoclax and are expected to live two to four months on average. The results demonstrated high response rates overall and in these venetoclax failed patients’ median OS was 59% at one year and thirty-two percent at two years. Our collaboration with the NCI under the CRADA could provide broad support for late-stage development of Actimab-A + CLAG-M and also other clinical trials to broaden use of Actimab-A. Actimab-A, if approved, would enable us to launch a second product that is complementary to Iomab-B and fulfill our ambition of transforming the treatment outcomes of r/r AML and expand our commercial footprint into the remaining top 100 cancer care centers outside of the leading BMT hospitals. |

20

| ● | Expand the Iomab-B label and revenue stream via life cycle management: We intend to leverage data from several clinical trials that demonstrate the ability of Iomab-B to improve BMT access and outcomes in five additional hematologic indications. These data in MDS, ALL, HL, NHL and MM provide the foundation to expand the label for Iomab-B and increase its market potential. In AML, we would seek label expansion into haploidentical transplants, earlier lines of treatment and younger patients below the age of 55, the cutoff in the SIERRA trial. As much as possible, we would seek to use investigator sponsored trials as the primary strategy for label expansion in order to maximize capital utilization. |

| ● | Further expand our conditioning franchise by developing Iomab-ACT for cell and gene therapies: We plan to develop Iomab-ACT to be used for either lymphodepletion or reduced intensity conditioning prior to CAR-T and gene therapies. Similar to BMT, access and outcomes of patients who might benefit from these therapies is limited by sub-optimal chemotherapy-based conditioning agents. The number of patients potentially eligible for Iomab-ACT is growing with increased availability of commercial cell and gene therapy products, as well as the expanding number of indications. We are studying Iomab-ACT in conditioning prior to CAR-T cellular therapy via a National Institutes of Health (“NIH”) funded clinical trial with Memorial Sloan Kettering Cancer Center (“MSKCC”). We expect to present proof-of-concept data from this study in the second half of 2023 and announce further development of this program in the CAR-T space. |

| ● | Leverage our R&D capabilities and technological prowess to advance our solid tumor programs and partnerships: We intend to continue to direct our R&D effort to advance our solid tumor programs into the clinic and support life cycle management for Iomab-B and Actimab-A. Our solid tumor programs and technological capabilities are validated by our partnerships with Astellas, LG Chem, and EpicentRx, which are focused on solid tumors and immunotherapies. Our R&D capability is demonstrated by our patent portfolio with over 200 issued and pending patent applications worldwide which include protection for Iomab-B into 2037. Our IP portfolio also includes several patent families to manufacture Ac-225 in a cyclotron and includes valuable know-how. |

| ● | In keeping with our strategic vision over the next five years, we plan to first focus on ensuring an Iomab-B approval and successful launch into core BMT centers to support commercial success. We intend to expand the Iomab-B label and revenue stream while progressing the development of Actimab-A by leveraging the NCI CRADA. We will progress the development of Iomab-ACT to proof-of-concept and explore potential partnerships as a means to achieve commercialization. Our solid tumor programs will progress toward the clinic as we continue to build out our commercial footprint into the top 100 hospitals leaving us positioned to develop them in line with our vision. With commercial dynamics aligning favorably for a successful Iomab-B launch and with late-stage development of Actimab-A in collaboration with the NCI, we plan to deliver on our mission to transform the treatment of AML and patient outcomes, and create a highly differentiated, specialty radiotherapeutics company focused on the top 100 large hospitals. |

21

Our Product Pipeline

We have strategically focused our development efforts in areas where there is a significant unmet medical need. We are developing a portfolio of novel radiotherapeutics that has the potential to positively impact the outcomes of people living with hard-to-treat diseases such as r/r AML via both a therapeutic and induction/conditioning agent. Outside of AML, our pipeline development offers the opportunity to enhance the value proposition of cell and gene therapies with our targeted conditioning programs.

AML Focused Programs – Iomab-B and Actimab-A

Our Iomab-B and Actimab-A product candidates are focused on addressing the major unmet medical needs in r/r AML in a complementary manner and are directed at different parts of the patient journey.

Iomab-B – Targeted Radiotherapeutic for Induction and Conditioning. A potential new standard of care enabling a curative BMT in currently non-transplantable r/r AML patients with poor survival prognosis

Opportunity to Change the Current Paradigm for Accessing a BMT and Improving Outcomes

The current approach in preparing patients for a BMT is to first induce a remission with therapeutic agents to reduce the disease burden and then suppress or destroy the patient’s immune system, including the diseased bone marrow, with conditioning regimens prior to transplanting the healthy donor hematopoietic stem cells, which are expected to restore normal bone marrow function following engraftment. As this approach requires patients to withstand multiple challenges from non-targeted therapies, which include chemotherapy agents and/or total body irradiation that are highly toxic, BMT is typically limited to FIT patients. Iomab-B is a targeted therapy that provides both disease control and conditioning in one agent and is well-tolerated even by UNFIT patients who typically are not transplanted in routine practice today. The SIERRA trial was designed to demonstrate that UNFIT patients with active disease could be administered Iomab-B and proceed directly to a BMT without the need for inducing a remission and that this approach could result in improved survival and curative outcomes. As seen by the positive results of the SIERRA trial detailed below, Iomab-B represents an exciting new paradigm in the management of AML patients and establishes a potential new standard of care especially for UNFIT patients in the relapsed or refractory setting.

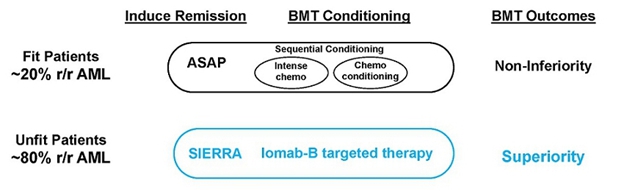

A similar approach has also been tried in the Phase 3 ASAP trial but with FIT patients. However, to avoid confusion between the potential of the approaches used in the ASAP and SIERRA trials, important distinctions between these trials are depicted in the graphic below. The ASAP trial sought to demonstrate non-inferiority between two non-novel approaches and found that outcomes similar to those of current practice could be achieved without first getting a patient into remission before taking them to BMT by giving them sequential conditioning or treating them twice with non-targeted chemotherapy agents that are typically used in this setting.

The ASAP approach is limited to only FIT patients as the UNFIT patients treated in SIERRA could not tolerate ASAP’s highly toxic sequential conditioning approach. Sequential conditioning is not novel as a similar trial to ASAP was conducted by the UK National Cancer Research Institute in 2019, which did not show any benefit from this approach in high-risk AML and MDS patients (Craddock et al. Augmented Reduced Intensity Regimen Does Not Improve Postallogeneic Transplant Outcomes in Acute Myeloid Leukemia. J Clin Oncol. 2021). The SIERRA trial results therefore can change the paradigm in transplant because non-transplantable patients in routine clinical practice can benefit from a transplant with Iomab-B and have superior outcomes. While both approaches in these trials support increased access to BMT, only Iomab-B is applicable to the unfit patients who comprise approximately 80%of r/r AML patients and can potentially expand the market for transplant.

22

Schetelig et al. Results from the Randomized Phase III ASAP Trial. ASH 2022

Pivotal Phase 3 SIERRA Trial for Iomab-B (131Iodine-apamistamab)

The SIERRA trial was designed to demonstrate the ability of Iomab-B to overcome challenges related to patient access to curative BMT. Unfortunately, approximately 30% of patients with AML have primary refractory disease while 50% relapse quickly after achieving initial remission. Getting these patients with primary r/r AML into remission is very challenging due to characteristics such as age, comorbidities, and disease features such as high-risk mutations that contribute to lack of response to salvage therapies and limit treatment options.

Patients must be able to overcome several challenges related to curative BMT. The first access challenge is that the patient needs to be in complete remission prior to BMT. The current clinical practice is not to transplant patients with active AML as outcomes are poor due to high relapse rates. The National Comprehensive Cancer Network (“NCCN”) guidelines also recommend treatment to achieve remission prior to transplant in patients with relapsed AML. The second challenge to access is tolerance to current conditioning regimens. For older patients, myeloablative regimens are not an option due to intense toxicity and mortality. The third challenge is the ability to achieve post-BMT remission and successful engraftment. Inadequate conditioning can lead to graft failure, which is associated with very high mortality. Patients who fail to achieve a CR post-transplant have extremely poor outcomes and a survival of a few weeks. The fourth challenge relates to BMT tolerability and post-BMT complications. The conditioning and immunosuppressive regimens given to these patients put them at high risk for infectious complications and toxicity. In the SIERRA trial, Iomab-B addresses all four of these challenges. Access to BMT is improved as CR is not needed pre-BMT given effective disease control and targeted myeloablation. With better post-BMT engraftment, CR and lower complications, the SIERRA trial also addressed the challenges related to improved outcomes through Iomab-B.

The SIERRA results, presented in the late-breaker session at the 2023 Tandem Meetings: Transplantation & Cellular Therapy Meetings of the ASTCT and the CIBMTR, support Iomab-B’s value proposition of enabling both improved access and outcomes of a BMT, thereby providing a significant curative option for r/r patients, a segment that represents approximately 50% of all AML patients and the majority not transplanted today. The design of the SIERRA trial is provided in the figure below.

23

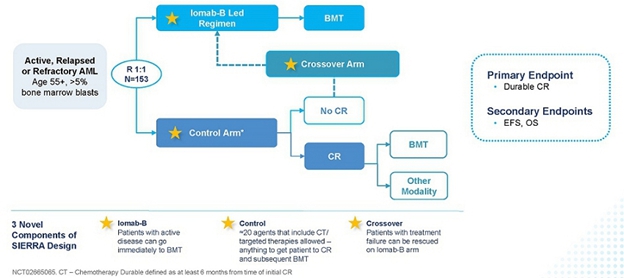

SIERRA: A Novel, Pivotal Phase 3 Study of Iomab-B in r/r AML

The pivotal Phase 3 SIERRA trial is a 153-patient, randomized, multi-center, controlled trial of Iomab-B in patients aged 55 and above with active r/r AML, who were heavily pre-treated and had high-risk characteristics. Patients enrolled had blast counts of 5% or greater in the marrow or circulating blasts suggestive of active AML. In this study, Iomab-B was compared to the control arm that allowed physician’s choice of over 20 available agents, including chemotherapies and/or targeted therapies such as venetoclax (BCL-2 inhibitor), FLT3 inhibitors, IDH inhibitors and Mylotarg, reflecting current best treatment practices attempting to get patients to CR. The control arm included recently approved AML therapies that were added to the SIERRA protocol as they became available. The crossover arm was designed in SIERRA for an equipoise that offered Iomab-B to patients failing to achieve a CR on the control arm with an intent to rescue them by taking them to transplant. Of note, SIERRA had highly restrictive optionality for post-transplant maintenance. Patients with active, r/r AML are not considered eligible for BMT with current approaches and the SIERRA trial was the only randomized Phase 3 trial to offer BMT as a treatment option for this patient population. These patients would not be offered BMT in standard practice and therefore have dismal survival outcomes of two to three months. The primary endpoint of the SIERRA trial was dCR of 180 days and the secondary endpoints are OS and Event-Free Survival (“EFS”). The comparison of OS in subjects randomized to the control arm who crossed over to receive Iomab-B versus all others in the control group was an exploratory efficacy endpoint.

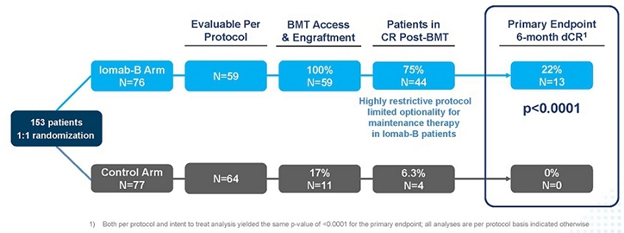

As seen in the graphic below, the primary endpoint of 6-month dCR was met with a high degree of statistical significance (p<0.0001). 75% of patients (44/59) receiving Iomab-B achieved an initial remission 30 days after their BMT compared to 6.3% of patients (4/64) in the control arm. 22% of the patients receiving Iomab-B maintained dCR lasting 180 days or more despite limited optionality for post-transplant maintenance, while none of the patients on the control arm achieved dCR. The current standard practice is to administer post-transplant maintenance therapy to reduce chances of relapse. The results presented below are on a per protocol basis, which means that only data that was in strict adherence to the protocol without any deviations was considered for the analysis. It is important to note that the p-value of the primary endpoint in the Intent-to-Treat (“ITT”) analysis was <0.0001, the same as the per protocol analysis.

24

SIERRA Results: Iomab-B Meets Primary Endpoint with High Significance (p<0.0001)

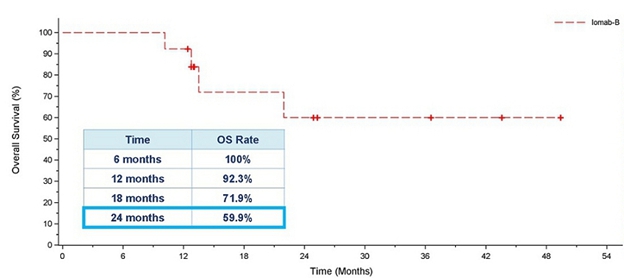

As demonstrated in the OS graph below, patients who achieved 6-month dCR had 92.3% 1-year survival and 59.9% 2-year survival. Median OS had not been reached in these patients. It is worth noting that two years in CR is a significant milestone in this patient population, highly indicative of long-term survival and a possible curative outcome.

Overall Survival for Patients who Achieved 6-month dCR with Iomab-B

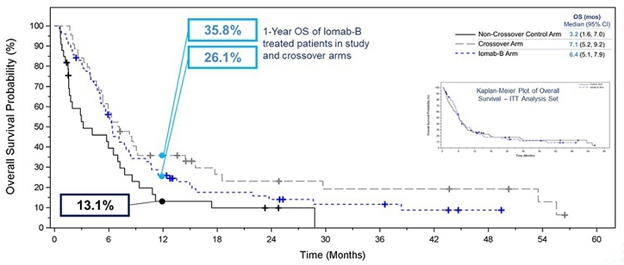

OS was one of the secondary endpoints of the study. The Kaplan-Meier plot in the inset of the graph below shows ITT OS results between the Iomab-B arm and the control arm. Due to the crossover design, ITT analysis of OS was confounded by the early crossover of patients (within 28 days) from the control arm to the Iomab-B arm (57.1%). The effective rescue of these crossover patients by Iomab-B led to an outsized contribution of the Iomab-B effect on control arm patients. As a result, median OS in the Iomab-B arm was similar to that in the control arm and this secondary endpoint was not met in the ITT analysis.

In order to isolate the true impact of Iomab-B on OS, one of the exploratory efficacy endpoints was the comparison of OS in subjects randomized to the control arm who crossed over to receive Iomab-B versus all others in the control arm, as well as the control arm patients who did not crossover versus the Iomab-B arm. The Kaplan-Meier plot of OS in the graphic below shows that this exploratory analysis demonstrated the clear benefit of Iomab-B over the control arm. The median OS for the Iomab-B group was 6.4 months which was double the 3.2 months for the non-crossover patients in the control arm. Patients who crossed over from the control arm to receive Iomab-B had a median OS of 7.1 months demonstrating further the ability of Iomab-B to treat patients who are non-treatable by conventional means.

25

A similar pattern favoring the Iomab-B group was seen across the pre-defined subgroups, where 1-year OS for Iomab-B was 26.1% compared with 13.1% for the non-crossover control arm. The 1-year OS for patients in the crossover arm was 35.8%. This clearly demonstrates the OS benefit of Iomab-B over the control arm and two to three-fold improvement in survival outcomes possible with its use.

Kaplan-Meier Plot of Overall Survival ‒ Iomab-B, Crossover, and Non-Crossover Control Arm

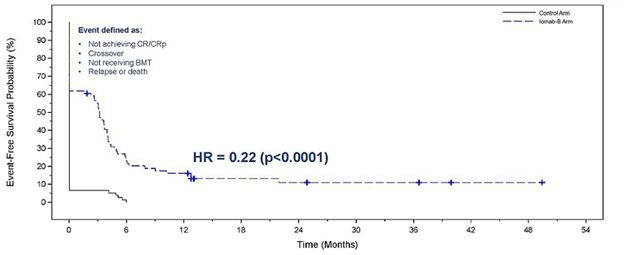

Iomab-B produced a significant and clinically meaningful improvement in the secondary endpoint of EFS, with a 78% reduction in the probability of an event (Hazard Ratio=0.22, p<0.0001 for both per protocol and ITT basis). EFS at 180 days for the Iomab-B arm was 28% compared to 0.2% for the control arm. In the SIERRA trial, an event is defined as one of the following: a patient not achieving CR/CRp or crossing over, patient not receiving BMT, a patient relapsing or death.

In the figure below comparing EFS with Iomab-B versus the control arm, the initial vertical drop in the curve in the Iomab-B arm represents those patients who did not achieve a remission after Iomab-B or those who did not proceed to transplant, while the initial vertical drop in the curve in the control arm mainly represents patients who did not achieve a remission with salvage therapy and either crossed over to Iomab-B or went onto best supportive care.

Event-Free Survival with Iomab-B Versus Control Arm

26

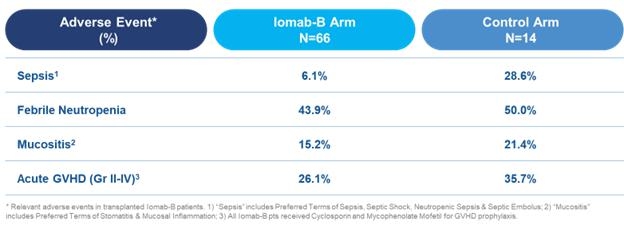

The table below shows relevant adverse events in transplanted Iomab-B patients. In these patients, incidence of sepsis was four times lower in the Iomab-B arm than the control arm (6.1% vs. 28.6%). In addition, rates of other treatment related adverse events were lower in favor of Iomab-B, including febrile neutropenia (43.9% vs. 50.0%), mucositis (15.2% vs. 21.4%) and acute graft versus host disease (“GVHD”) (26.1% vs. 35.7%).

Grade ≥3 Treatment-Emergent Adverse Events in Transplanted Patients Through Day 100 Post-HCT

With current treatment practice, patients who have r/r AML with active disease, utilizing current conditioning agents have poor outcomes and very low survival rates. Using an Iomab-B led regimen, an unprecedented number of patients were able to access transplant and were able to do so with active disease, eliminating need for achieving a CR in order to transplant the patient. Thus, patients are also able to access BMT faster with Iomab-B, in less than half the time compared to conventional care. Iomab-B represents an exciting new paradigm with the potential to establish a new standard of care in r/r AML setting, making it possible for most patients to get to a successful transplant with Iomab-B with a portion of these patients having a long-term survival benefit. As shown below, with an Iomab-B led regimen, the majority of patients who are non-transplantable in routine clinical practice can be successfully transplanted, administering myeloablative radiation with reduced intensity conditioning tolerability to ultimately achieve transformative survival outcome, changing the treatment paradigm for r/r AML patients.

Iomab-B – New Paradigm to Upend BMT Access and Improve r/r AML Outcomes

27

Future Development and Life Cycle Management for Iomab-B

The results of the Pivotal Phase 3 SIERRA trial validate the value proposition of Iomab-B, and we believe it could establish unprecedented access to transplant (currently the only curative option) with better safety and tolerability and improved outcomes, all of which could potentially make Iomab-B the new standard of care for patients with r/r AML. We are actively working to launch an EAP and successfully file a BLA in the second half of 2023, and if approved, we anticipate the commercial launch for Iomab-B in 2024.

We intend to commercialize Iomab-B in the U.S. The commercial opportunity is supported by favorable dynamics, summarized by the “Three Ps and Two Cs”:

| ● | Patients: With its promising profile, Iomab-B provides the opportunity for unprecedented BMT access and better outcomes for patients, with favorable safety and tolerability |

| ● | Physicians: Our goal is to help physicians make BMT an option for a vast majority of r/r AML patients who currently are unable to access transplant without disruption to current practice. Patients are able to return to their referring physicians for post-BMT follow-up, long-term care |

| ● | Payers: Iomab-B potentially unlocks value through getting patients safely to effective, potentially curative transplants, with improved outcomes and a manageable safety and tolerability profile |